What Is Money Laundering, and Why Do Companies Worry About It?

Money laundering is the process criminals use to make “dirty” money (proceeds of illegal activity) appear legitimate. Without checks, illicit cash can flow through everyday financial products like loans, investments, and trading. funding terrorism, drug cartels, fraud, and corruption.

Money laundering is the process criminals use to make “dirty” money (proceeds of illegal activity) appear legitimate. Without checks, illicit cash can flow through everyday financial products such as loans, investments, and trading. Funding terrorism, drug cartels, fraud, and corruption.

Laundering typically happens in three stages:

- Placement: Criminals inject cash into the financial system, splitting large sums into smaller deposits or buying goods convertible back into cash.

- Layering: Funds move through multiple transactions, often across borders and through shell companies, to obscure their origin.

- Integration: “Cleaned” money re-enters the economy via legitimate assets: property, businesses, or even more financial products.

Unchecked, these activities distort markets, undermine the rule of law, and expose everyday users like you to the risk of fraud, identity theft, or service disruptions.

Why AML Matters for Businesses and the Economy

- Protecting Individuals & Businesses: AML programs help detect suspicious activity early, stopping fraudsters who might otherwise hijack your account, drain your investments, or misuse your identity.

- Maintaining Market Integrity: Imagine laundered funds manipulating stock prices, or criminals using micro-loan platforms to funnel illicit cash. AML controls preserve fair prices and ensure you’re competing on a level playing field.

- Safeguarding Trust in Financial Services: When a major platform is fined for AML lapses, trust erodes. Strong AML frameworks prevent service shutdowns, fines, or negative headlines, keeping your favourite apps available and credible.

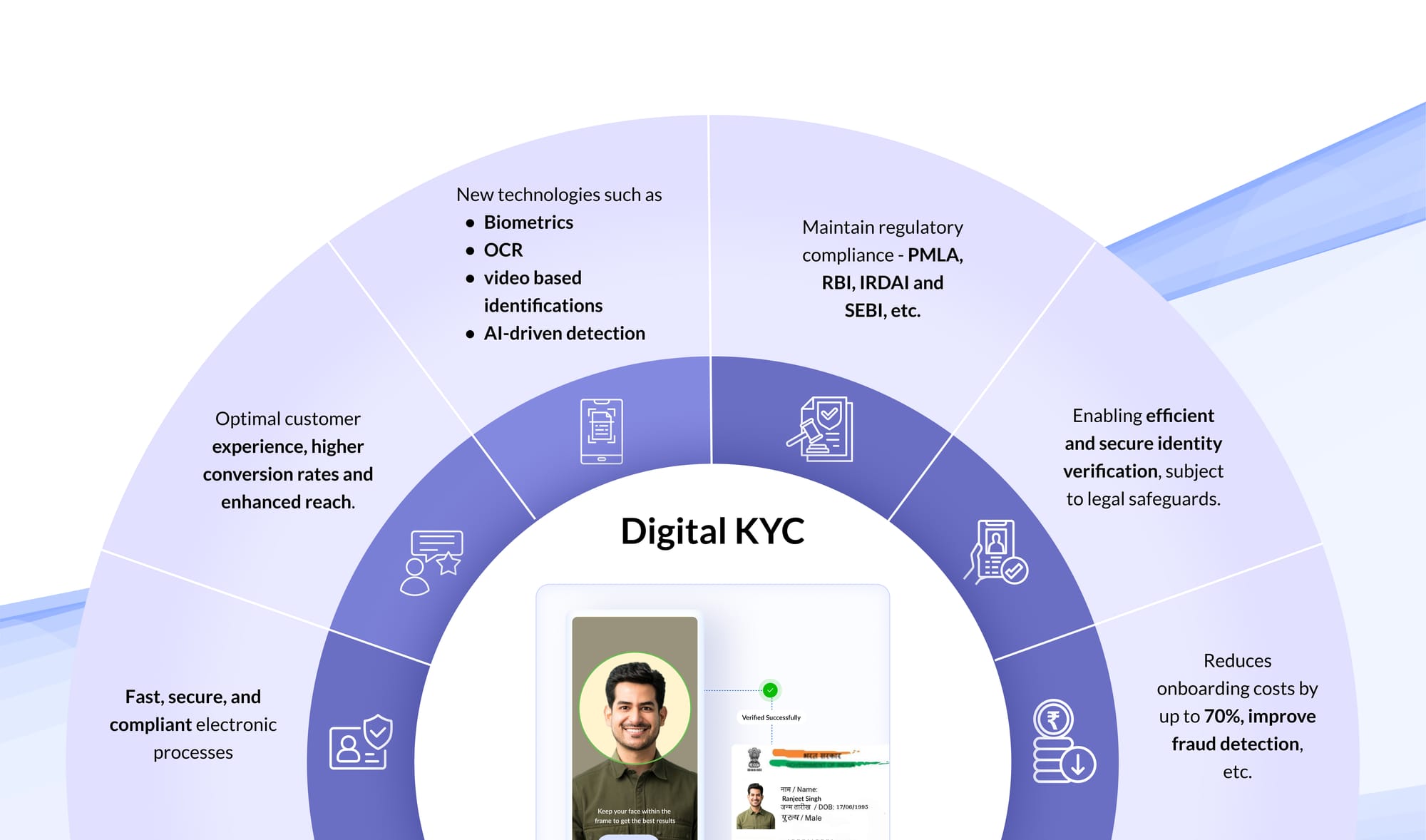

- Meeting Legal & Regulatory Requirements In India, AML obligations flow from the Prevention of Money Laundering Act (2002) and RBI’s Know Your Customer (KYC) Master Direction (2016). Non-compliance risks heavy penalties, license restrictions, and even criminal liability costs that ultimately can end up as higher fees or reduced services for users.

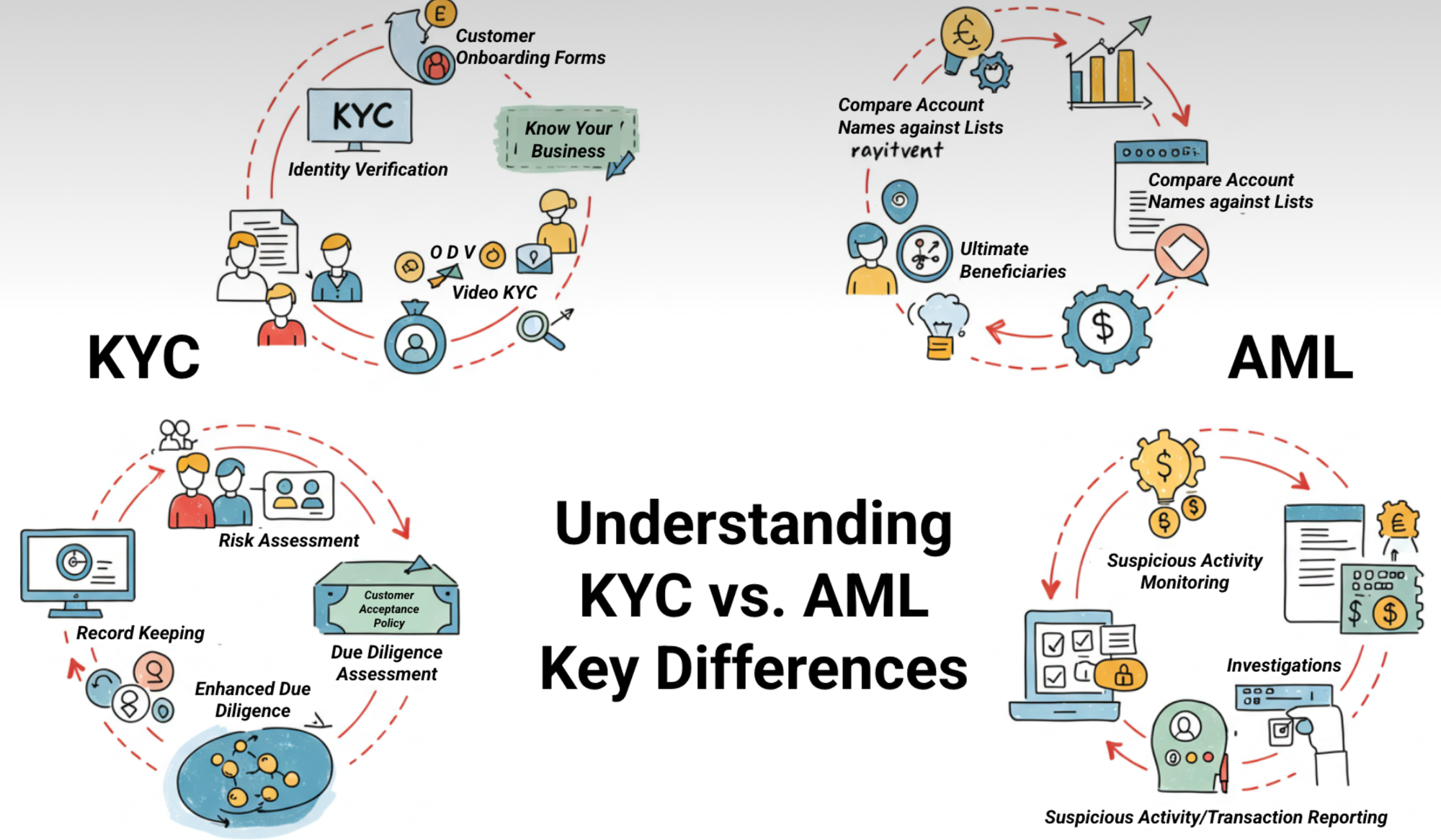

The Four Pillars of an Enterprise AML Program

Whether you’re a retail user or a fintech founder, AML rests on four core activities:

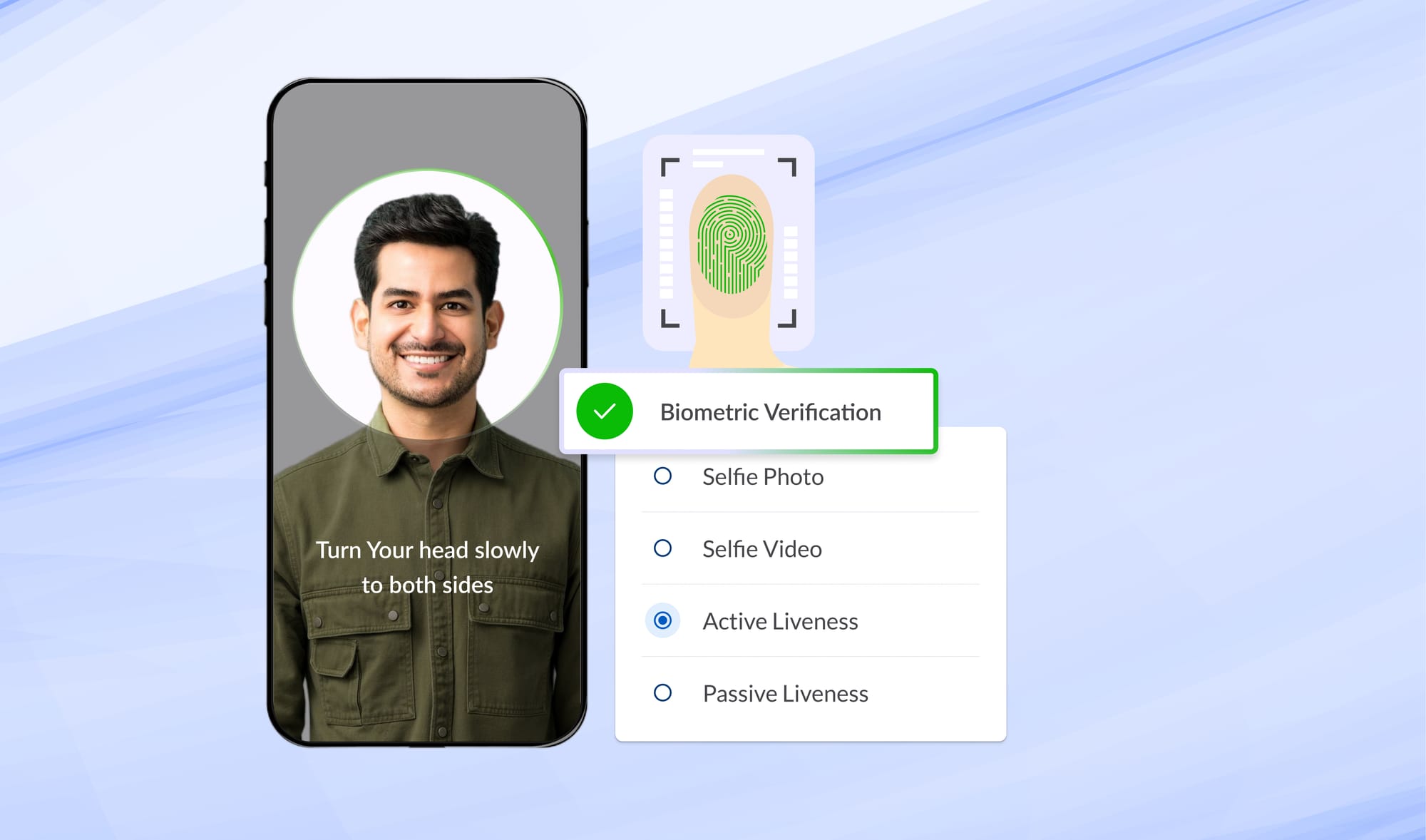

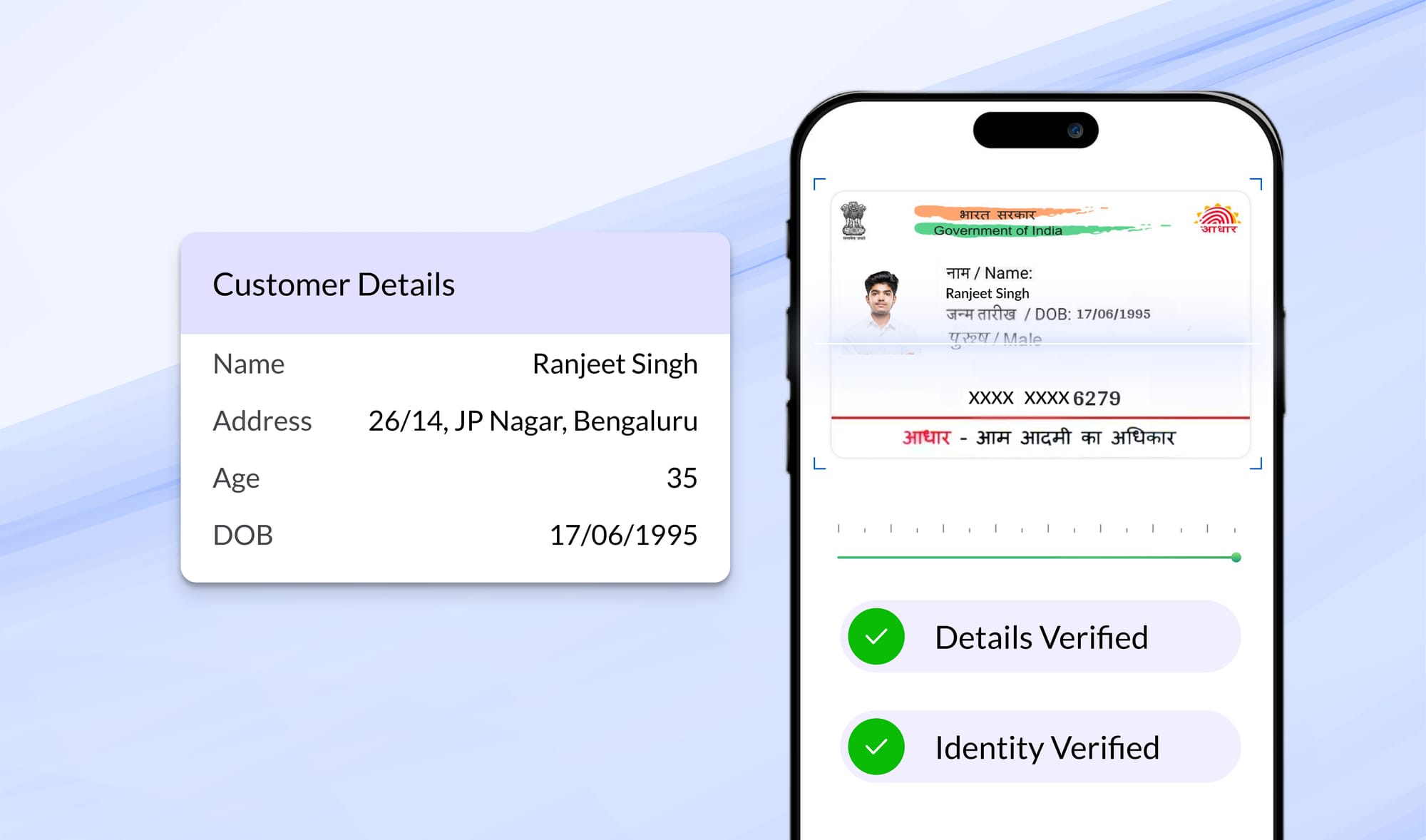

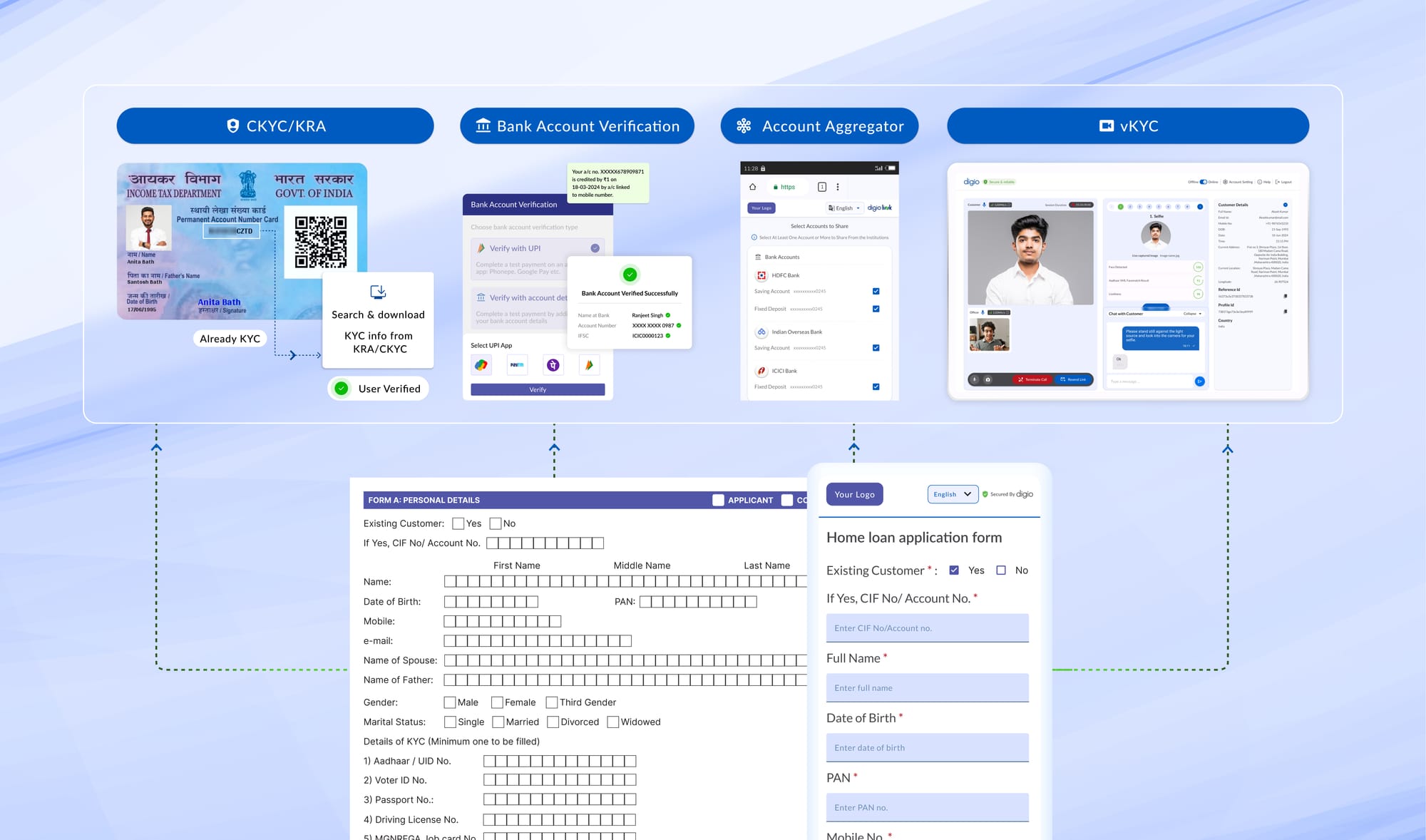

1. Know Your Customer (KYC)

Before you can detect risk, you must verify identity. KYC involves:

- Identity Checks: Validating government IDs (Aadhaar, passports) or electronic equivalents.

- Biometric Verification: Selfie-based liveness tests to confirm the person matches the furnished identity document.

- Basic Risk Profiling: Assigning customers a low/medium/high risk rating based on factors like geography, occupation, and transaction intent.

These steps ensure that every user is who they say they are and establish a foundation for ongoing monitoring.

2. Customer Due Diligence (CDD) & Enhanced Due Diligence (EDD)

Not every customer poses the same risk.

- Standard CDD covers routine transactions, small SIPs, and retail payments, applying automated checks and basic risk scoring.

- EDD kicks in for higher-risk profiles:

- Politically Exposed Persons (PEPs)

- Transactions above defined thresholds (e.g., large loan disbursements)

- Customers in high-risk jurisdictions

EDD involves deeper investigations into a customer’s source of funds, ownership structures, and ongoing periodic reviews.

3. Ongoing Monitoring

Onboarding is just the start:

- Watchlist Screening: Customers and transactions are re-screened regularly against global sanctions, PEP, and adverse-media lists.

- Transaction Surveillance: Automated systems flag patterns like rapid velocity, structuring (many small transactions), or transfers to high-risk countries.

- Alert Investigation: When a rule or model triggers an alert, compliance teams review details and determine if further action, such as filing a report, is needed.

4. Suspicious Transaction Reporting (STR) & Record Keeping

When genuine red flags emerge, firms must file Suspicious Transaction Reports with the Financial Intelligence Unit, India, within seven days of forming suspicion. Simultaneously, every screening event, rule change, and investigation note is logged and archived, often for at least five years, ensuring a clear audit trail for regulators or internal reviews.

Which entities are subject to AML compliance?

Not every app with a payments button needs a full-blown AML program. In India, the Prevention of Money Laundering Act (PMLA) lays down the law. It applies to a wide class of institutions that qualify as Reporting Entities. These include:

- Banks and NBFCs: Whether you're a large commercial bank or a nimble digital lending platform offering short-term credit.

- Payment System Operators: Wallets, UPI apps, and platforms that facilitate money movement—even if they don’t hold deposits.

- Mutual Fund Distributors & Asset Managers: If your platform allows investment into debt or equity instruments, you’re covered.

- Stock Brokers & Investment Portals: Apps offering demat services, equity trades, or even fractional investing fall under the compliance radar.

- Prepaid Instrument Issuers: Including neobanks and fintechs offering virtual cards or stored-value wallets.

- Crypto Exchanges (increasingly regulated): As guidelines tighten, VASPs (Virtual Asset Service Providers) are being brought under formal AML rules.

- Insurance Intermediaries: Platforms offering life, health, or even micro-insurance products are also on the list.

If your business model involves facilitating money inflows, fund transfers, or investment routes, odds are you fall under AML obligations. Even if you're not a traditional financial institution, once you touch customer funds or sensitive financial data, regulators expect you to implement controls.

AML in Everyday Life: What customers experience

Quick Yet Thorough Onboarding: Customers complete e-KYC in under two minutes because identity checks and watchlist screenings run in parallel.

- Occasional Document Requests: Large transactions (say, a high-value loan drawdown) may trigger “Please share supporting financial documents” prompts. It may feel inconvenient, but it’s a sign the platform is doing its job.

- Transaction Delays: Transfers above certain limits or to new beneficiaries sometimes take a few extra hours for enhanced review. This protects the business and the network from fraud.

- Transparent Fees & Disclosures: To maintain robust AML teams and technologies, some platforms charge a nominal “compliance fee”. This money goes towards sustaining these essential safeguards.

Who Sets the Rules, and How They’re Enforced

- International Standard-Setters: The FATF publishes global AML/CFT recommendations, including the Risk-Based Approach (FATF Recommendation 1) that encourages flexible, proportionate enforcement.

- Local Regulators: In India, RBI’s KYC Master Direction (2016) and the Prevention of Money Laundering Act (2002) define specific obligations for banks, NBFCs, and fintechs.

- Financial Intelligence Unit–India (FIU-IND): The national agency that receives STRs, analyzes trends, and shares actionable intelligence with law enforcement.

Platforms face periodic audits by regulators or independent examiners to verify that policies are board-approved, controls are in place, and records are complete.

Evolution of AML technologies

As fintech innovations accelerate, AML evolves too:

- Digital Identity & Decentralized KYC: Blockchain-based IDs and zero-knowledge proofs promise faster, more secure verifications, reducing friction for users.

- Machine Learning Surveillance: Beyond static rules, AI models detect subtle, emerging laundering patterns in real time, adapting faster than manual rule updates.

- Collaborative Data Sharing: Fintech consortia can anonymously share aggregated risk indicators, raising collective defenses against new threat frontiers.

For customers and businesses alike, staying informed about AML developments ensures they can seize fintech’s benefits, speed, convenience, and innovation without exposing themselves or their digital footprints to unintended risks.

Conclusion

Every time customers engage with financial services, they rely on AML controls working silently in the background. From verifying their identity in seconds to helping businesses file timely reports on suspicious flows, AML is the financial world’s immune system protecting customers, markets, and economies from the hidden costs of crime. Understanding its basics helps everyone appreciate why that extra document request or brief delay isn’t red tape, but a vital safeguard keeping the system sound.

Read more Blogs

DPDP Consent Management: What Every Data Fiduciary Must Know in 2026

How DPDP consent management works: consent capture, lifecycle, consent managers, and what data fiduciaries must implement before May 2027.

DPDP Compliance Platform: Complete Guide for Indian Enterprises (2026)

Everything Indian enterprises need to know about choosing a DPDPA compliance platform: features, deployment options, timelines, and penalties. Updated for 2026.

DPDP Compliance for Banks: A CISO's 90-Day Roadmap

Indian banks sit at the intersection of two regulatory forces: the Reserve Bank of India's Data Governance Guidelines and the Digital Personal Data Protection Act, 2023. With full DPDPA enforcement beginning May 13, 2027, and penalties reaching ₹250 crore, banks face the highest compliance stakes of any sector. The challenge isn't just regulatory, it's operational. Banks handle tens of millions of data principals across dozens of digital properties (mobile apps, net banking, UPI, loan portals,

Digitally transform business operations with Digio!

Try first. Subscribe later.

Boost your legal ops efficiency by 80%

Learn how Digio can enhance your business productivity

Get 1-on-1 business use case solutioning

Speak with our business consultants to get a solution walkthrough for your business requirement

Test the APIs

Let your development team test our API suite to understand configurability and product integration

Subscribe

Get the best in industry commercials for your business usecase