DPDP Consent Management: What Every Data Fiduciary Must Know in 2026

How DPDP consent management works: consent capture, lifecycle, consent managers, and what data fiduciaries must implement before May 2027.

Consent is the cornerstone of India's Digital Personal Data Protection Act.

Unlike GDPR, which offers six legal bases for processing personal data, the DPDPA makes consent the primary legal basis for most data processing activities.

If you process personal data of Indian citizens, you need a consent management system, not as a nice-to-have, but as a regulatory mandate with ₹250 crore penalties behind it.

This guide covers what DPDP requires for consent, the difference between a Consent Management Platform (CMP) and a registered Consent Manager, the non-negotiable features, and how to implement consent management before the May 2027 enforcement deadline.

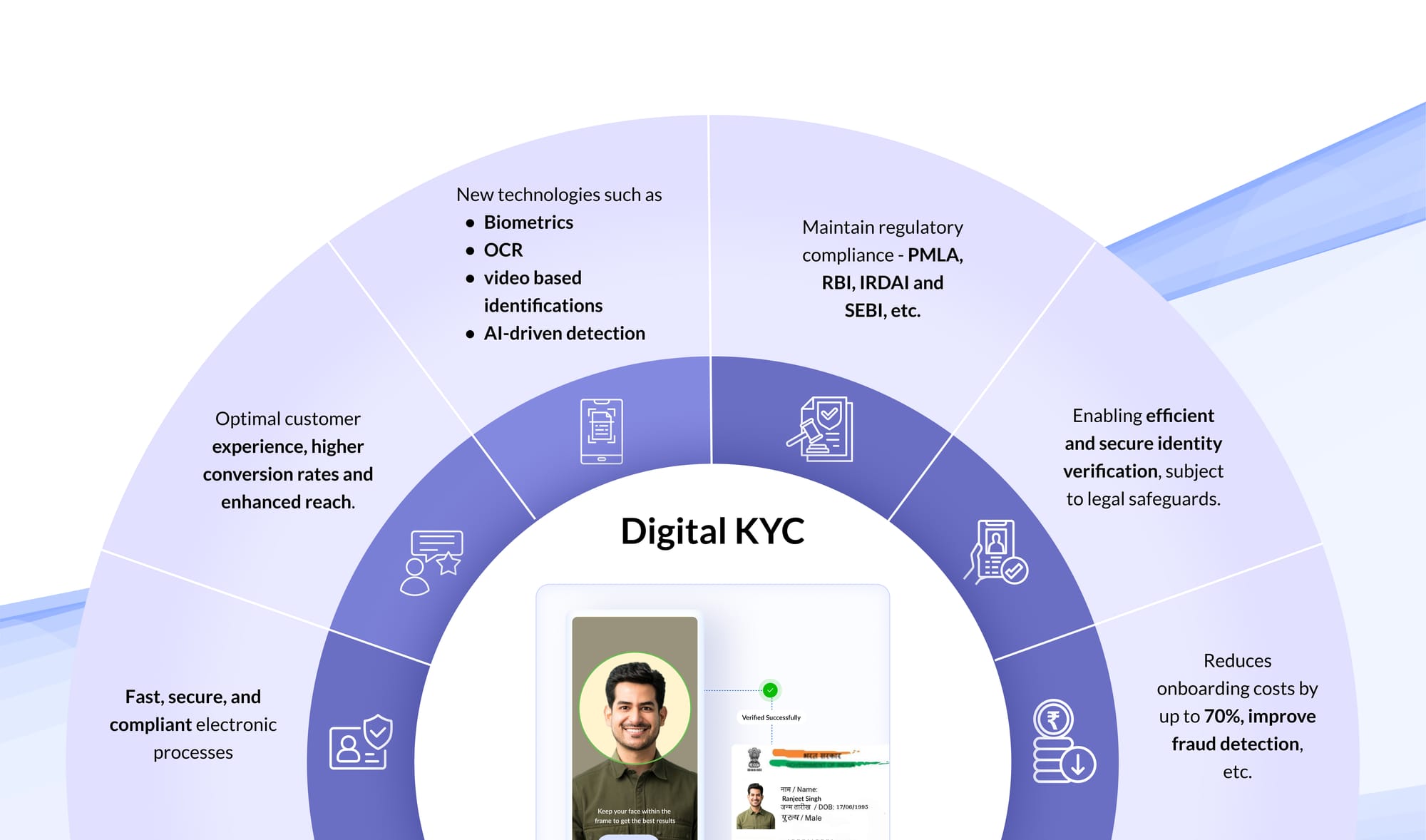

What the DPDP Act Requires for Consent

The DPDPA establishes a consent framework that is significantly more prescriptive than most global privacy laws.

Here are the key requirements:

Section 6(1): Free, Specific, Informed, Unconditional

Consent must be:

- Free: Not coerced or bundled with service access

- Specific: Tied to a defined purpose (no blanket consent)

- Informed: Preceded by a clear privacy notice in the user's language

- Unconditional: Not contingent on accepting unrelated terms

- Unambiguous: Captured through an affirmative action (OTP, toggle, explicit opt-in)

This means you cannot bury consent in a Terms & Conditions page; each data processing purpose requires separate, explicit consent.

Section 5(1) & 5(3): Privacy Notices

Before collecting consent, you must present a privacy notice that clearly states:

- What personal data is being collected

- Why is it being collected (specific purpose)

- How the data principal can exercise their rights

This notice must be available in all 22 languages listed in the Eighth Schedule of the Constitution: Hindi, Tamil, Telugu, Kannada, Bengali, Marathi, Gujarati, Malayalam, and 14 others.

Section 6(4): Withdrawal Must Be As Easy As Giving Consent

This is one of the most consequential provisions. If your user gave consent with a single tap, they must be able to withdraw it with a single tap. Complex withdrawal processes are a violation.

Your system must provide:

- A Privacy Centre or Preference Centre accessible to every data principal

- One-click revocation per processing purpose

- Immediate downstream effect when consent is withdrawn, processing must stop

Section 8(7) & 12(3): Right to Erasure

When consent is withdrawn, the data fiduciary must erase the data principal's personal data, not just stop processing it, but actually delete it across all systems, databases, and third-party processors.

This requires deep integration between your consent management system and your data infrastructure.

Consent Management Platform vs Consent Manager

These two terms are often confused. They are fundamentally different:

Key insight: You need a Consent Management Platform now to be compliant. Consent Managers are a future ecosystem layer that won't be operational until late 2026.

Don't wait for Consent Managers, build your consent infrastructure today.

Features Your Consent Management System Must Have

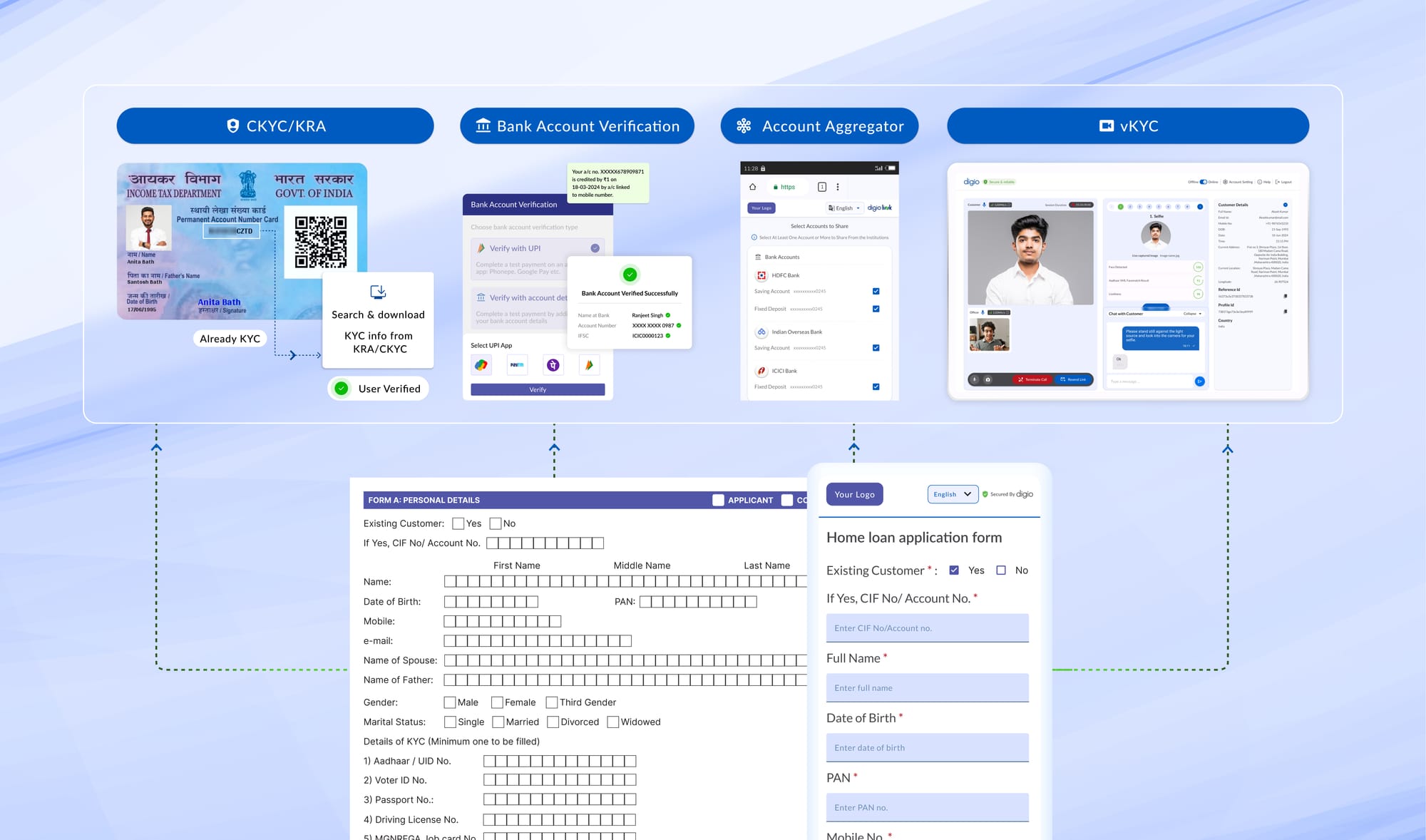

1. Granular Purpose-Level Consent

Each processing purpose must have its own consent capture. Your system must support independent opt-in/opt-out per purpose: "Account Opening", "Marketing", "Credit Assessment", "Third-Party Sharing" should each be separate toggles, not a single "Accept All" button.

2. Multilingual Consent Notices

22 Indian languages are mandated under Section 5(3). Your CMP must either auto-translate or allow manual translation of every privacy notice. The user should be able to switch language and read the full notice in their preferred language before consenting.

3. Immutable Consent Artifacts

Every consent decision must generate a tamper-proof record: who consented, when, to what, which version of the notice they saw, their IP address, device fingerprint, and a cryptographic hash (SHA-256) that invalidates if the record is altered. This is your forensic evidence in case of a regulatory audit.

4. Consent Withdrawal Infrastructure

A Privacy Centre or Preference Centre where data principals can:

- View all active consents

- Revoke any consent with one click

- Download their consent history

- File a grievance

5. Webhook-Driven Downstream Enforcement

When consent is withdrawn, your CMP must notify all downstream systems in real-time. This means webhook/API integration with your CRM, marketing automation, analytics, data warehouse, and third-party processors. Consent revocation must trigger actual processing stops, not just a flag update in a database.

6. SDK for Seamless Integration

For web and mobile apps, the CMP should provide lightweight SDKs (React, Angular, iOS, Android) that your engineering team can embed with minimal code. The SDK handles consent capture UI, language selection, and API calls to the backend.

7. Cookie Consent Management

For websites, the CMP must detect and classify cookies (strictly necessary, analytics, marketing), present a compliant consent banner, and block non-essential cookies until consent is granted.

BFSI vs Fintech vs Enterprise: Different Needs

Pricing Models: How Consent Management Platforms Charge

Understanding the pricing model is critical because costs can vary 3-5x depending on the model:

Tip: Always calculate 3-year TCO, not just the Year-1 price. Factor in implementation fees, AMC (for on-premise), overage charges, and communication costs (SMS/WhatsApp/email for notifications).

Explore CoTrust: DPDPA Consent Management Platform by Digio

Frequently Asked Questions

Q: What is DPDP consent management?

A: DPDP consent management refers to the systems and processes organisations use to capture, store, manage, and enforce user consent as required by India's Digital Personal Data Protection Act, 2023.

It involves presenting clear privacy notices, obtaining purpose-specific consent, maintaining immutable records, enabling easy withdrawal, and ensuring consent decisions are enforced across all data processing systems.

This is mandatory for every entity processing personal data of Indian citizens.

Q: What is the difference between a consent management platform and a consent manager?

A: A Consent Management Platform (CMP) is software that organisations deploy to manage consent internally. It handles consent capture, storage, withdrawal, and audit.

A Consent Manager, as defined under the DPDPA, is a registered entity (with a minimum net worth of ₹2 crore) that acts as a neutral intermediary between data principals and multiple data fiduciaries.

Consent Manager registration opens November 13, 2026. Organisations need a CMP now; Consent Managers are a future ecosystem layer.

Q: Which consent management platforms work for Indian banks?

A: Indian banks require platforms that support on-premise or private cloud deployment (for data residency), field-level encryption, WORM audit logs, 22 Indian language support, and integration with core banking systems.

The platform must support both RBI compliance requirements and DPDPA obligations simultaneously.

Key evaluation criteria include deployment flexibility, security certifications, and proven banking deployments.

Q: How much does consent management cost in India?

A: Costs depend on the pricing model and deployment type.

SaaS platforms range from ₹15-40 lakh per year for typical enterprise volumes.

On-premise deployments for banks range from ₹28-80 lakh per year plus implementation fees.

Pricing models vary; some charge per data principal per month (₹0.02-0.04), others per consent event, and others per digital property. Always calculate 3-year TCO, including implementation, AMC, and overage charges, before comparing.

This content is for informational purposes and does not constitute legal advice. Consult qualified legal professionals for advice specific to your circumstances.

Read more Blogs

DPDP Consent Management: What Every Data Fiduciary Must Know in 2026

How DPDP consent management works: consent capture, lifecycle, consent managers, and what data fiduciaries must implement before May 2027.

DPDP Compliance Platform: Complete Guide for Indian Enterprises (2026)

Everything Indian enterprises need to know about choosing a DPDPA compliance platform: features, deployment options, timelines, and penalties. Updated for 2026.

DPDP Compliance for Banks: A CISO's 90-Day Roadmap

Indian banks sit at the intersection of two regulatory forces: the Reserve Bank of India's Data Governance Guidelines and the Digital Personal Data Protection Act, 2023. With full DPDPA enforcement beginning May 13, 2027, and penalties reaching ₹250 crore, banks face the highest compliance stakes of any sector. The challenge isn't just regulatory, it's operational. Banks handle tens of millions of data principals across dozens of digital properties (mobile apps, net banking, UPI, loan portals,

Digitally transform business operations with Digio!

Try first. Subscribe later.

Boost your legal ops efficiency by 80%

Learn how Digio can enhance your business productivity

Get 1-on-1 business use case solutioning

Speak with our business consultants to get a solution walkthrough for your business requirement

Test the APIs

Let your development team test our API suite to understand configurability and product integration

Subscribe

Get the best in industry commercials for your business usecase