DPDP Compliance for Banks: A CISO's 90-Day Roadmap

Indian banks sit at the intersection of two regulatory forces: the Reserve Bank of India's Data Governance Guidelines and the Digital Personal Data Protection Act, 2023. With full DPDPA enforcement beginning May 13, 2027, and penalties reaching ₹250 crore, banks face the highest compliance stakes of any sector. The challenge isn't just regulatory, it's operational. Banks handle tens of millions of data principals across dozens of digital properties (mobile apps, net banking, UPI, loan portals,

Indian banks sit at the intersection of two regulatory forces: the Reserve Bank of India's Data Governance Guidelines and the Digital Personal Data Protection Act, 2023.

With full DPDPA enforcement beginning May 13, 2027, and penalties reaching ₹250 crore, banks face the highest compliance stakes of any sector.

The challenge isn't just regulatory, it's operational. Banks handle tens of millions of data principals across dozens of digital properties (mobile apps, net banking, UPI, loan portals, wealth management platforms). Each touchpoint collects personal data. Each requires DPDPA-compliant consent.

This roadmap gives CISOs and DPOs a 90-day action plan to achieve DPDP compliance, accounting for the unique complexity of banking infrastructure.

Why Banks Face the Highest DPDP Risk

Banks are disproportionately exposed because of:

- Scale: Top banks have 10-50 crore data principals. At ₹250 crore max penalty, the regulatory exposure per bank is existential.

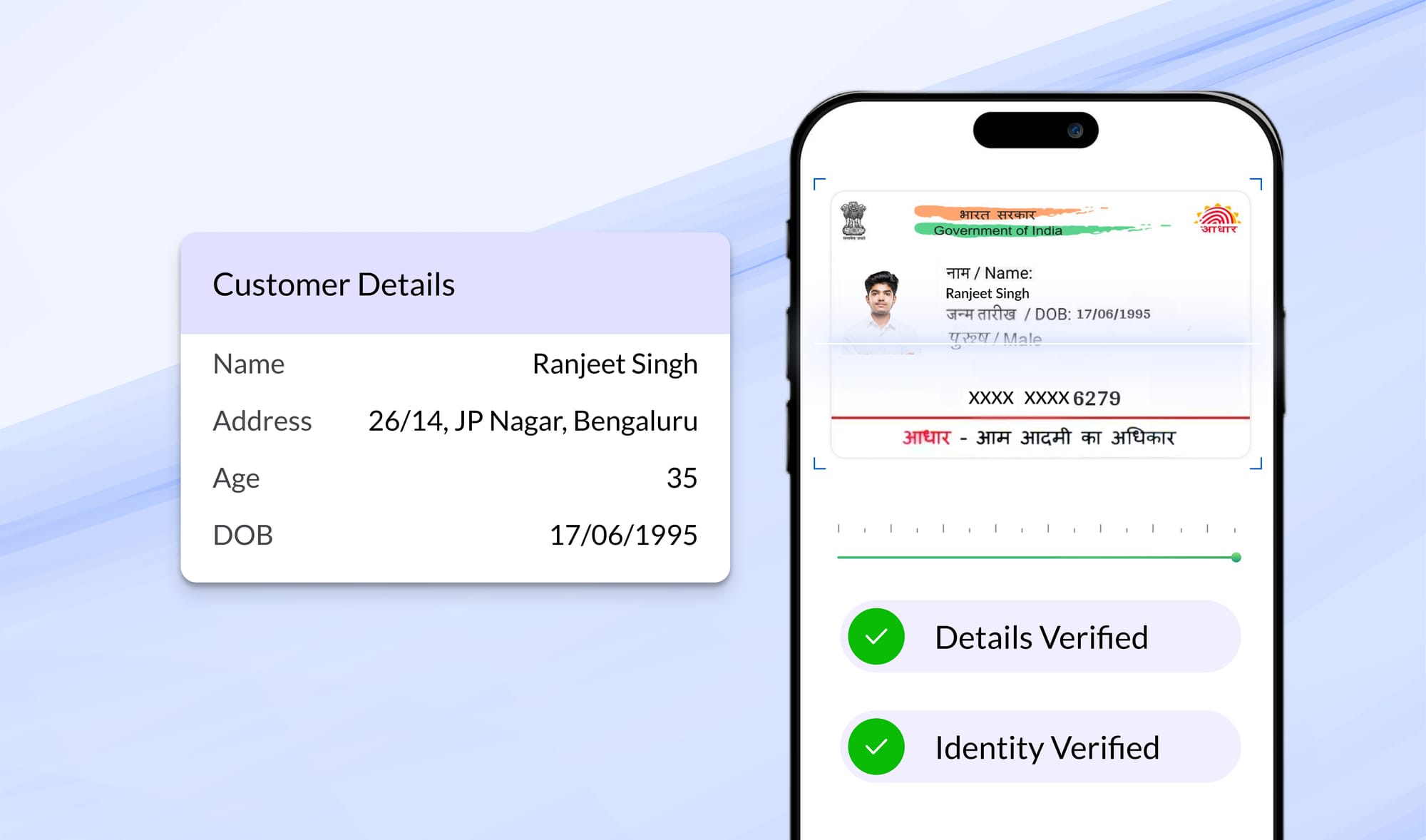

- Data Sensitivity: Financial data (account numbers, PAN, Aadhaar, credit scores) is among the most sensitive personal data categories.

- Multiple Digital Properties: A typical bank has 15-20+ digital touchpoints - mobile app, internet banking, UPI, loan origination systems, wealth platforms, insurance distribution, ATM data, call recordings. Each needs consent capture.

- Third-party processors: Banks share data with credit bureaus (CIBIL, Experian), payment processors, KYC aggregators, marketing partners, and IT vendors. Under DPDPA, the bank remains liable for how processors handle data.

- Dual regulation: Banks must comply with both RBI data governance circulars and DPDPA simultaneously. These frameworks overlap but don't always align.

A mid-size bank with 5 crore customers, 16 digital properties, and 50+ third-party data processors faces a compliance surface area that no manual process can manage. This is why consent management technology is not optional for banking.

The 90-Day Compliance Roadmap

Phase 1: Data Audit & Gap Analysis (Day 1-30)

Objective: Understand what personal data you have, where it lives, and what consent gaps exist.

Week 1-2: Data Mapping

- Inventory all systems that store or process personal data (core banking, CRM, data warehouse, marketing tools, call recording systems)

- Classify data by category: name, contact details, financial data, identity documents (PAN, Aadhaar), biometric, transaction history

- Map data flows: which systems share data with which? Where does data leave the bank's perimeter?

- Identify all third-party processors and the data they access

Week 3-4: Consent Gap Analysis

- For each data processing activity, identify: Is there documented consent? Is it purpose-specific? Is it withdrawable?

- Identify legacy data principals: users who signed up before DPDPA. Do you have valid consent under the new law?

- Map all digital properties and assess which ones have consent capture mechanisms vs which don't

- Document the gap between the current state and DPDPA requirements

Deliverable: A comprehensive Data Protection Impact Assessment (DPIA) document that your DPO can present to the board.

Phase 2: Consent Infrastructure (Day 31-60)

Objective: Deploy consent management technology across all digital properties.

Week 5-6: Platform Selection & Deployment

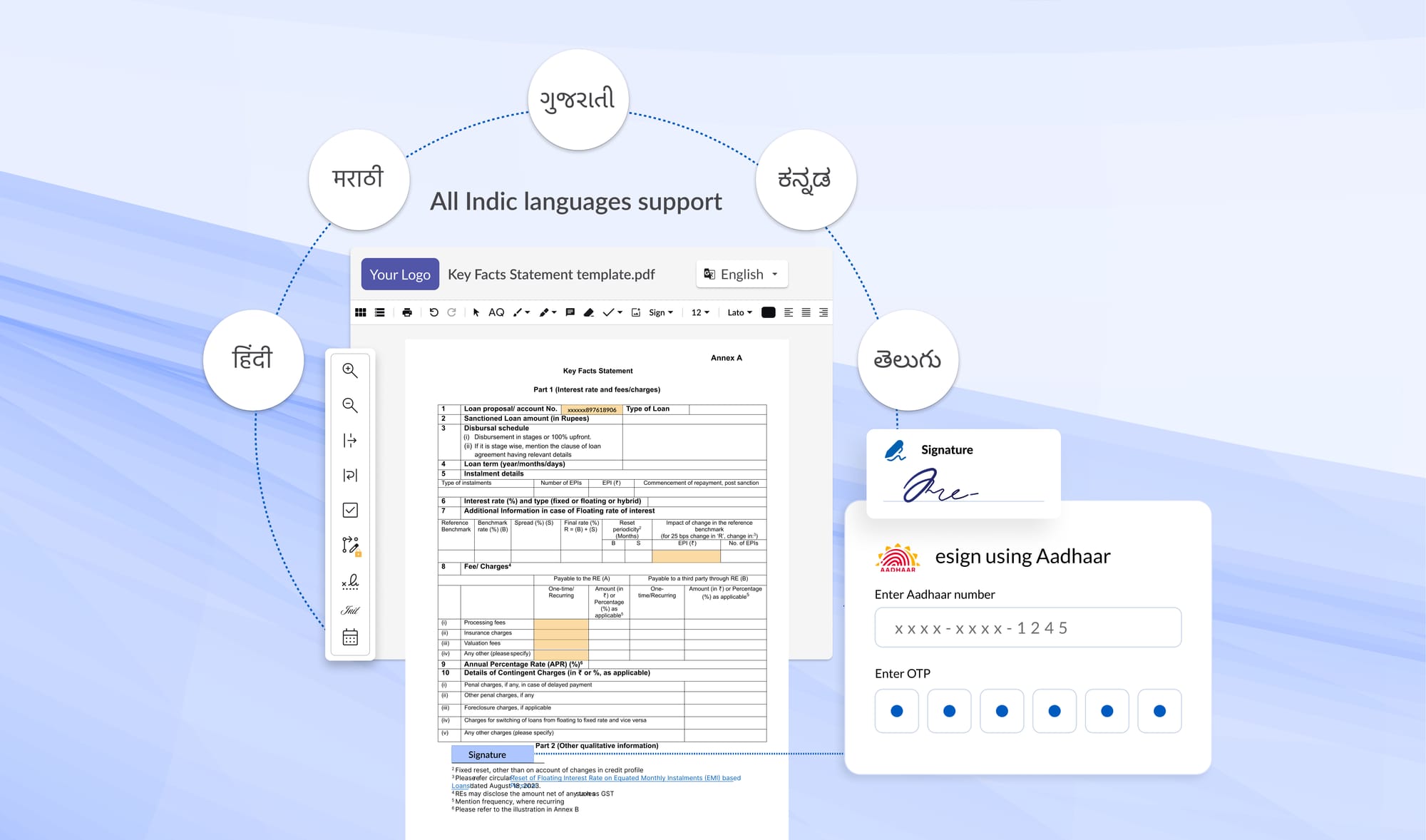

- Select a DPDPA consent management platform based on key criteria: on-premise support, 22 languages, immutable audit trail, SDK for mobile/web

- Deploy on bank infrastructure (on-premise or private cloud - most scheduled banks require this)

- Integrate with the core banking system via API/webhook

Week 7-8: Consent Capture Rollout

- Design privacy notices for each processing purpose (account opening, marketing, credit assessment, third-party sharing)

- Deploy consent capture SDK on all digital properties (mobile app, net banking, loan portals)

- Implement Privacy Centre/Preference Centre for users to manage their consents

- Set up legacy consent campaign: re-acquire consent from existing users via email/SMS/in-app notification

- Configure webhook-driven enforcement: consent withdrawal triggers processing stops in downstream systems

Deliverable: Consent management live on at least 3 primary digital properties. Privacy Centre accessible to all users.

Phase 3: Breach & DSR Readiness (Day 61-90)

Objective: Build the operational infrastructure for breach notification and data subject rights.

Week 9-10: Breach Notification Protocol

- Establish a 72-hour breach notification workflow: detection → assessment → DPB notification → data principal notification

- Pre-draft notification templates (for both the Data Protection Board and affected individuals)

- Integrate breach detection with consent platform: know exactly which data principals are affected and what consent they had

- Define escalation matrix: who detects, who assesses, who notifies, who communicates externally

Week 11-12: Data Subject Rights Automation

- Deploy DSR intake portal (web form, email, API endpoint for automated requests)

- Configure workflow routing: access requests → data team, erasure requests → DPO approval → deletion execution

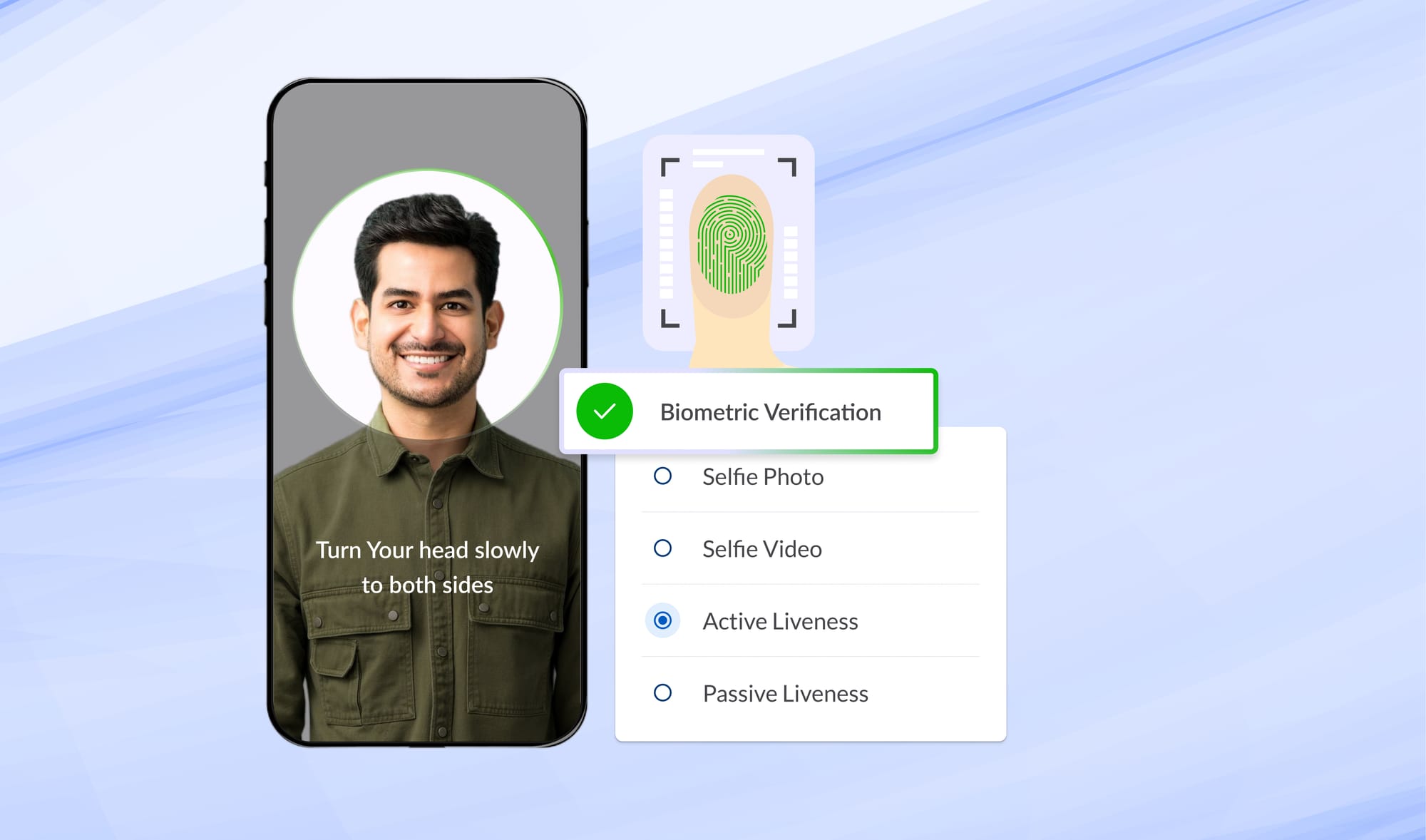

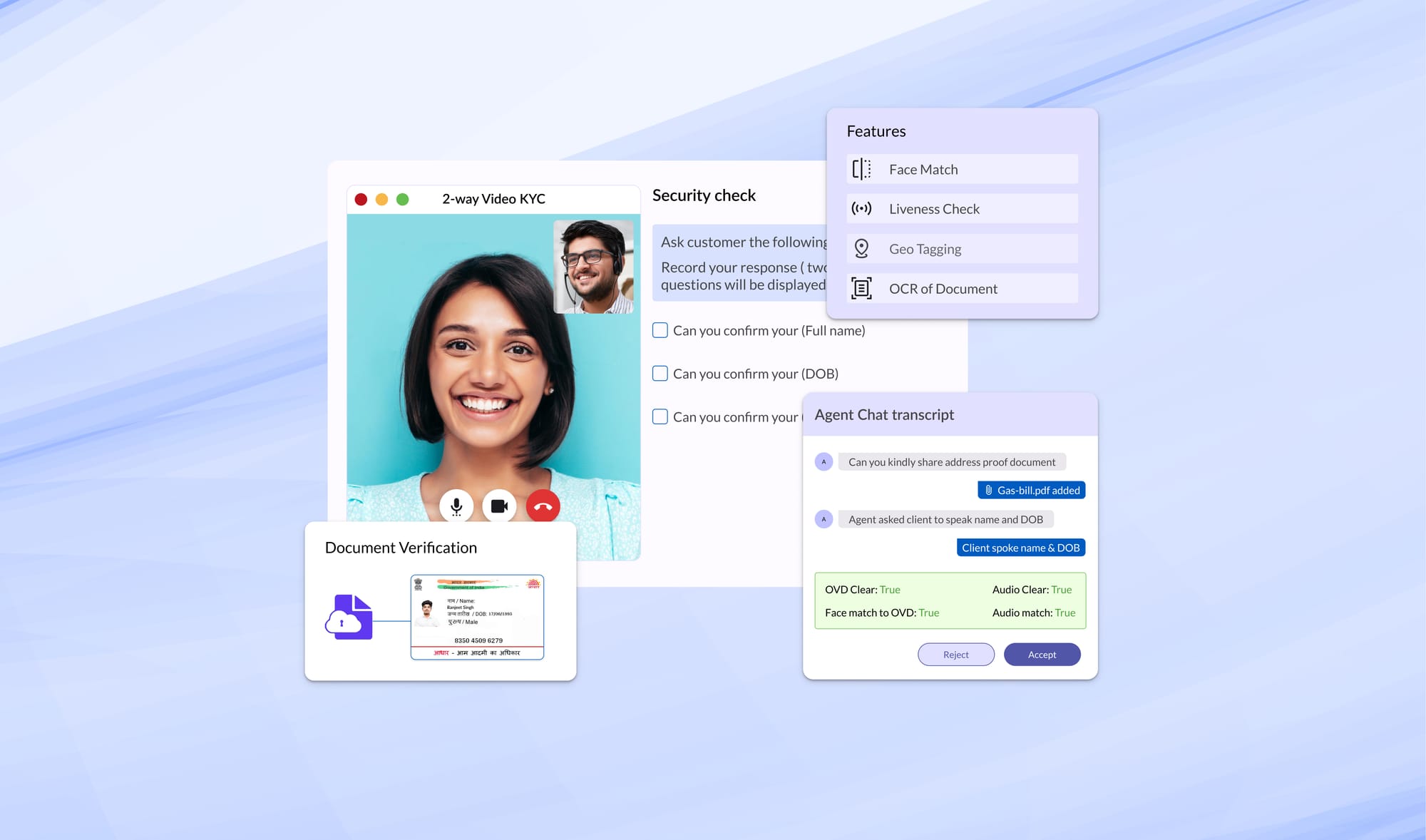

- Implement identity verification before fulfilling any DSR (OTP, in-app authentication)

- Test end-to-end erasure: can you actually delete a user's data across all systems within the SLA?

- Set up SLA monitoring: 7-day default for DSR fulfilment, with breach risk alerts

Deliverable: Breach notification workflow tested. DSR portal is live. End-to-end erasure capability demonstrated.

RBI Guidelines + DPDPA: Navigating Dual Compliance

Banks must navigate overlapping requirements from RBI and DPDPA:

Key insight: DPDPA doesn't replace RBI requirements; it adds to them. Banks need a consent management platform that can handle both frameworks simultaneously.

Choosing a Compliance Platform for Banking

Non-negotiable requirements for banks:

- On-premise deployment: scheduled commercial banks typically cannot use SaaS for compliance-critical systems

- Field-level encryption: PII fields must be encrypted at rest with bank-managed keys

- WORM audit logs: tamper-evident, forensic-grade audit trail for the Data Protection Board

- 22 Indian languages: banks with national presence must support all Schedule VIII languages

- Multi-zone high availability: active deployment across availability zones, consistent with bank IT standards

- Integration with core banking: APIs and webhooks that connect to existing CBS, CRM, and data warehouse

- Proven banking deployments: ask for references from banks of similar size and complexity

Explore CoTrust: Built for Indian banks, deployable on-premise

Frequently Asked Questions

Q: Is DPDPA compliance mandatory for Indian banks?

A: Yes. The Digital Personal Data Protection Act, 2023, applies to all entities processing personal data of Indian citizens, including all scheduled commercial banks, small finance banks, cooperative banks, NBFCs, and payment banks.

Full enforcement begins May 13, 2027, with penalties up to ₹250 crore per violation. Banks face additional compliance obligations under RBI data governance circulars, creating a dual compliance requirement.

Q: What is the DPDPA breach notification timeline for banks?

A: Under DPDPA, data fiduciaries (including banks) must notify the Data Protection Board and all affected data principals within 72 hours of becoming aware of a personal data breach.

This is in addition to existing CERT-In and RBI notification requirements. Banks should establish a unified breach response workflow with pre-drafted notification templates and a clear escalation matrix to meet all regulatory timelines simultaneously.

Q: Can DPDPA compliance platforms be deployed on-premise in bank infrastructure?

A: Yes. Several India-built DPDPA compliance platforms support on-premise or private cloud deployment, which is typically required for scheduled commercial banks under RBI's data governance framework.

On-premise deployment ensures all consent records, audit logs, and personal data remain within the bank's infrastructure.

Typical deployment takes 4-8 weeks, including integration with core banking systems. Annual maintenance charges (AMC) apply for on-premise deployments, covering upgrades, security patches, and L2/L3 support.

This content is for informational purposes and does not constitute legal advice. Consult qualified legal professionals for advice specific to your circumstances.

Read more Blogs

DPDP Consent Management: What Every Data Fiduciary Must Know in 2026

How DPDP consent management works: consent capture, lifecycle, consent managers, and what data fiduciaries must implement before May 2027.

DPDP Compliance Platform: Complete Guide for Indian Enterprises (2026)

Everything Indian enterprises need to know about choosing a DPDPA compliance platform: features, deployment options, timelines, and penalties. Updated for 2026.

DPDP Compliance for Banks: A CISO's 90-Day Roadmap

Indian banks sit at the intersection of two regulatory forces: the Reserve Bank of India's Data Governance Guidelines and the Digital Personal Data Protection Act, 2023. With full DPDPA enforcement beginning May 13, 2027, and penalties reaching ₹250 crore, banks face the highest compliance stakes of any sector. The challenge isn't just regulatory, it's operational. Banks handle tens of millions of data principals across dozens of digital properties (mobile apps, net banking, UPI, loan portals,

Digitally transform business operations with Digio!

Try first. Subscribe later.

Boost your legal ops efficiency by 80%

Learn how Digio can enhance your business productivity

Get 1-on-1 business use case solutioning

Speak with our business consultants to get a solution walkthrough for your business requirement

Test the APIs

Let your development team test our API suite to understand configurability and product integration

Subscribe

Get the best in industry commercials for your business usecase