DPDPA

DPDP Consent Management: What Every Data Fiduciary Must Know in 2026

How DPDP consent management works: consent capture, lifecycle, consent managers, and what data fiduciaries must implement before May 2027.

DPDPA

How DPDP consent management works: consent capture, lifecycle, consent managers, and what data fiduciaries must implement before May 2027.

DPDPA

Everything Indian enterprises need to know about choosing a DPDPA compliance platform: features, deployment options, timelines, and penalties. Updated for 2026.

DPDPA

Indian banks sit at the intersection of two regulatory forces: the Reserve Bank of India's Data Governance Guidelines and the Digital Personal Data Protection Act, 2023. With full DPDPA enforcement beginning May 13, 2027, and penalties reaching ₹250 crore, banks face the highest compliance stakes of any sector.

DPDPA

Step-by-step guide to building ROPA for DPDP compliance: templates, automation, and how consent governance feeds into your processing records.

DPDPA

Under DPDPA, data breaches must be reported within 72 hours. Learn who reports, what qualifies as a breach, and how to stay compliant.

Onboarding

Aadhaar verification in India has shifted from using physical copies to a digital, consent-driven model. This new approach minimizes data exposure, ensures accountability, and aligns with UIDAI and DPDP principles.

DPDPA

India’s DPDP Act makes legacy data a compliance hurdle. Learn to manage transition notices, build defensible audit trails, and understand why a Consent Manager is a vital risk-containment tool for your existing database.

DPDPA

India’s digital lending ecosystem is entering a decisive compliance phase. With the DPDP Rules notified and RBI mandates tightening, lenders and LSPs must rethink consent, data roles, legacy data, and governance frameworks ahead of the 2027 enforcement deadline.

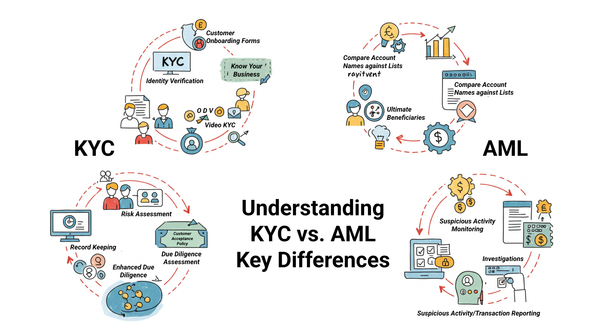

AML/CFT

Money laundering is the process criminals use to make “dirty” money (proceeds of illegal activity) appear legitimate. Without checks, illicit cash can flow through everyday financial products like loans, investments, and trading. funding terrorism, drug cartels, fraud, and corruption.

AML/CFT

KYC vs. AML, although they work hand-in-hand, each has its own scope, timing, and technical requirements. This article focuses on a concise breakdown to help businesses assess solutions against both requirements while remaining compliant.

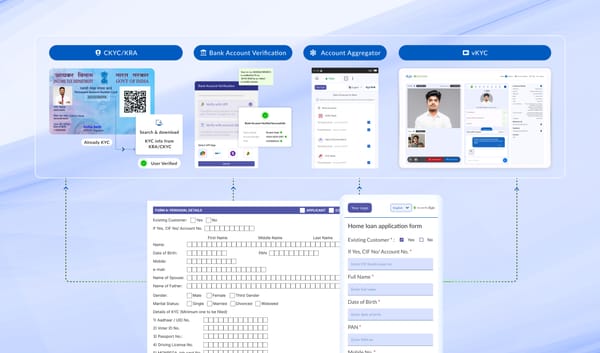

Onboarding

The biggest game-changer for Indian NBFC growth is faster onboarding and digital journeys supported by new technologies like the CKYC registry, automated bank account verification, bank-statement retrieval via Account Aggregator, video-based KYC, and UPI mandates.

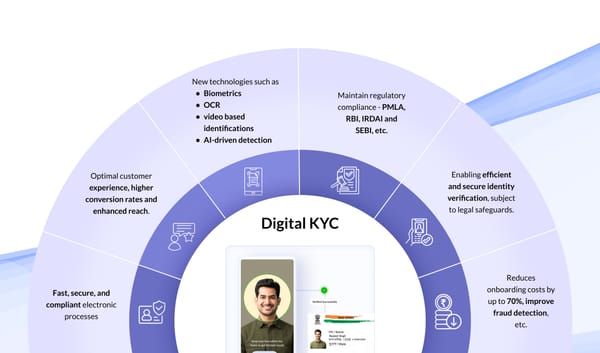

Onboarding

Digital KYC is an enabler for operational efficiency and regulatory compliance which allows businesses to transform their paper-based verification processes. This represents a paradigm shift in how customer identities are verified & financial crimes are mitigated in a completely electronic manner.